Since the topic is of great interest, a lot of information appears in the public space, which does not always accurately reflect the current legal status, often confusing the current national law with EU projects.

That is why we have prepared a short summary (as of 12 August 2025), which clearly presents the changes in ESG reporting according to CSRD in the context of Omnibus.

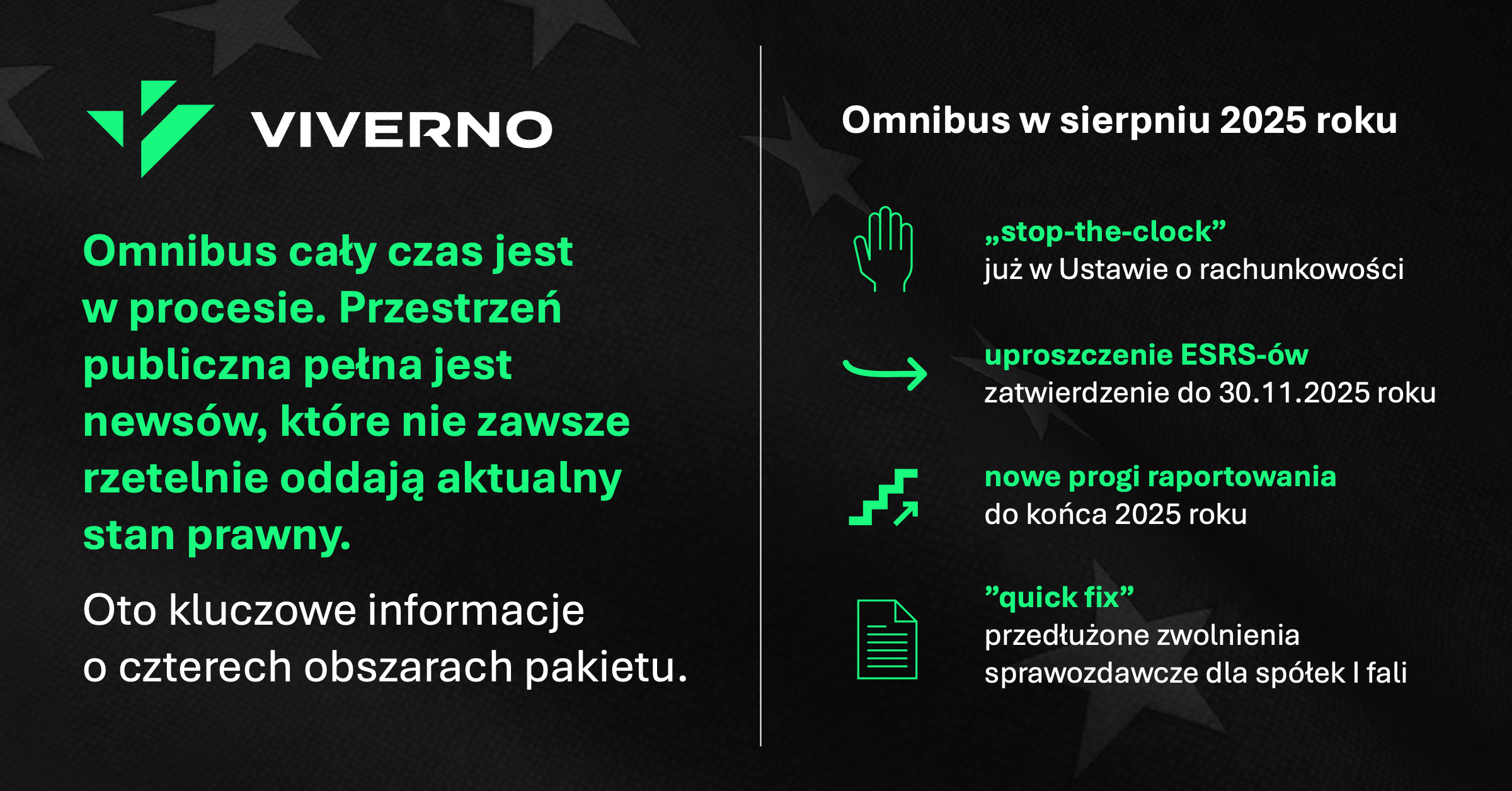

What do we know?

- In Poland, the Accounting Act has already been amended, which introduced the obligation to report ESG in December 2024. The presidential signature of July 23, 2025 implemented the so-called “stop-the-clock” mechanism, which postponed the deadline for mandatory reporting by 2 years for companies from the so-called II and III waves. These are large companies not listed on the stock exchange (second wave — employment of 250 people or more, at least PLN 110 million of total assets and at least PLN 220 million of annual net income) and SMEs listed on the stock exchange (III wave — more than 10 people employed, PLN 2 million of balance sheet total, revenues of PLN 4 million net per year).

- Work is underway to simplify ESRS standards — it is possible that their volume will be reduced by up to more than 50%. The changes are to be approved by November 30, 2025, and the first application will take place in 2027 (reports for 2026).

- In the second half of 2025, the announcement of new thresholds for companies covered by ESG reporting is expected. Trilateral negotiations (trialogue) between the European Commission, the European Parliament and the Council of the EU are currently underway.

- The companies of the so-called first wave (covered by the previous NFRD directive - already reporting on the ESRS for 2024) will most likely be able to benefit from the simplifications contained in the delegated regulation of July 2025 known as the “quick fix” in their reports for 2025 and 2026. In most cases, the “quick fix” extends the possibility of applying the simplifications provided for in Appendix C to ESRS 1 concerning the gradual implementation of disclosure requirements. This makes it possible, among other things, to temporarily omit the reporting of emissions in scope 3.

This is the situation for the middle of August 2025. We are closely following the progress of work on the Omnibus. We will keep you updated on the next steps related to the package. Let's stay in touch!

Our services as part of the ESG Report

We will prepare a report for your company that complies with all CSRD and ESRS guidelines, including double significance analysis.